What Is a Good Interest Rate on a Car Loan in 2026?

Answering: What Is a Good Interest Rate on a Car Loan in 2026?

Estimated reading time: 8 min read

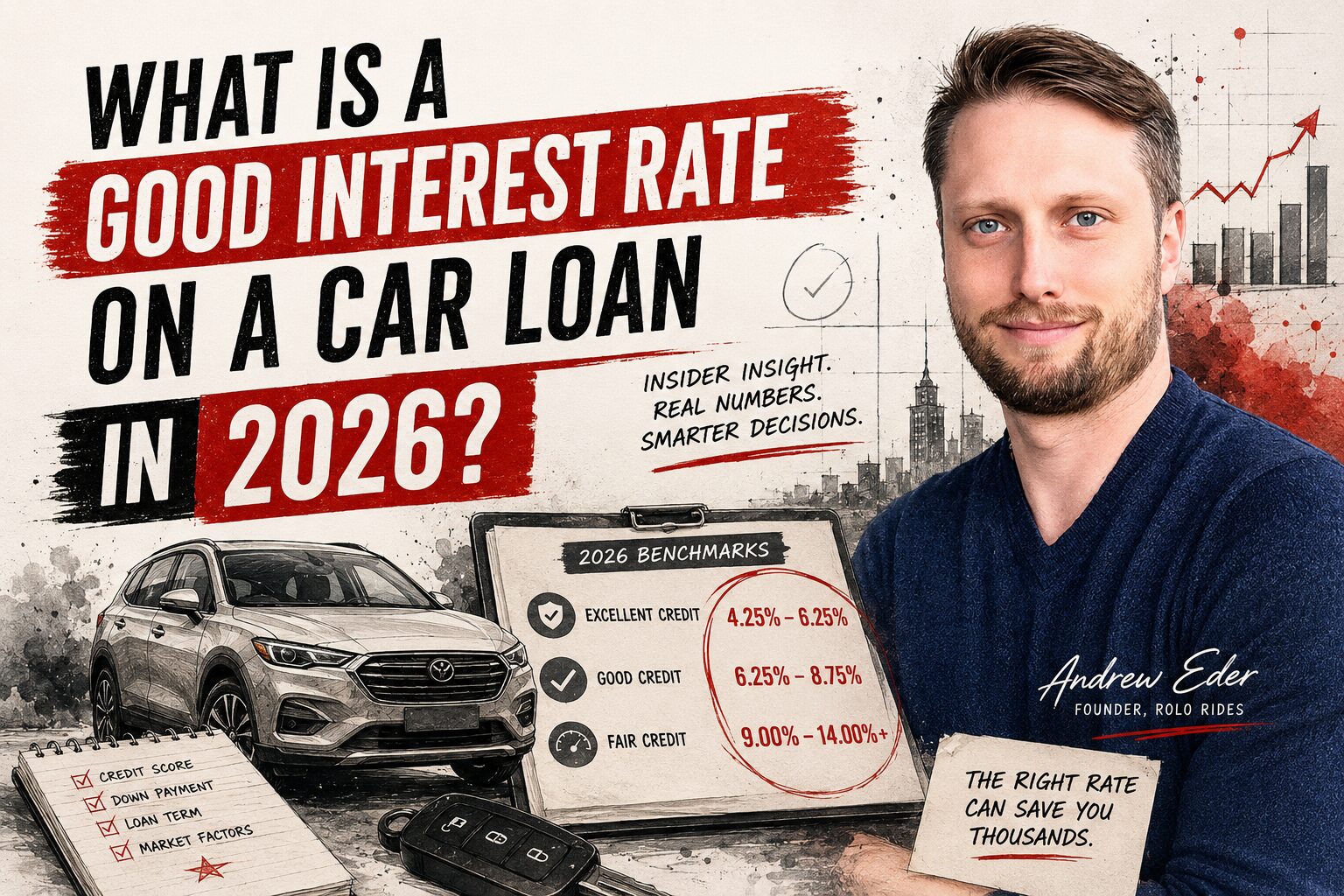

A good interest rate on a car loan in 2026 is below 5.5% for a new vehicle and below 7.5% for a used vehicle, assuming you have good to excellent credit (700+). The national average is approximately 7% for new car loans and 11% to 12% for used car loans on a 60-month term, according to Experian and Bankrate data from early 2026. But those averages include every credit tier, from super prime to deep subprime. If your credit score is above 700, you should be well below the average. If a dealer offers you a rate near or above the average and your credit is strong, the rate has likely been marked up. Rolo Rides founder Andrew Eder, who managed a dealership finance office, explains exactly how that markup works and what rate you should actually be paying.

Interest rates are one of the least understood costs in a car purchase. Most buyers focus on the vehicle price and monthly payment, but the interest rate determines how much you pay beyond the price of the car itself. On a $40,000 loan over 60 months, the difference between a 5% rate and a 7% rate is approximately $2,100 in extra interest. That is money that goes to the lender and the dealership, not toward the vehicle.

The challenge is that most buyers accept whatever rate the dealer presents without knowing whether it is competitive. An MIT analysis cited by NerdWallet found that 78% of dealer-arranged auto loans carry interest rates marked up above the lender's wholesale rate. The average markup is 1.13 percentage points, which means the rate you are offered at the dealership is almost certainly higher than the rate the lender actually approved for you. Understanding what a good rate looks like is the first step toward not overpaying.

This guide covers what rates to expect based on your credit score, how dealer rate markup works, and how to ensure you are getting the rate you actually qualify for.

Key Insights

- A good new car loan rate in 2026 is below 5.5% for buyers with credit scores above 700. The national average of approximately 7% includes all credit tiers and is not a benchmark for well-qualified buyers.

- The dealer's offered rate is not your actual rate. In 78% of dealer-arranged loans, the interest rate is marked up 1% to 2.5% above the lender's wholesale rate. Pre-approval from a bank or credit union reveals your real rate before the dealer has the opportunity to inflate it.

- On a $40,000 loan over 60 months, every 1% of rate markup costs you approximately $1,100 in extra interest. That cost is invisible because it is embedded in your monthly payment, not listed as a separate fee.

Keep reading for full details below.

The fastest way to know if your rate is fair: get pre-approved first, then compare.

Rolo Rides reviews the financing on every deal to ensure buyers are getting the actual lender rate, not a marked-up version. Andrew Eder managed the finance office where rates are marked up and knows exactly how to identify and eliminate the difference.

Table of Contents

- Key Insights

- What Rates to Expect by Credit Score

- How Dealer Rate Markup Works

- New vs. Used Car Loan Rates

- How to Get the Best Rate on Your Car Loan

- 2026 Car Loan Rate Reference Table

- Frequently Asked Questions

- Want to Learn More

- Citations

What Rates to Expect by Credit Score

Your credit score is the single biggest factor in determining your interest rate. Lenders use it to assess risk: the higher your score, the lower the rate they are willing to offer. Here is what you should expect in 2026 based on Experian's most recent automotive finance data.

Super prime (781+): Expect new car rates around 4.5% to 5.5% and used car rates around 5.5% to 7%. If you are in this tier and a dealer offers you anything above 6% on a new vehicle, the rate has almost certainly been marked up. This is the tier where markup is most profitable for the dealer because buyers assume their good credit is already reflected in the offered rate.

Prime (661-780): Expect new car rates around 5.5% to 7.5% and used car rates around 7% to 10%. This is the broadest credit tier and where most car loans fall. Rates vary significantly within this range, which means shopping between lenders (not just between dealers) can save hundreds or thousands in interest.

Near prime (601-660): Expect new car rates around 8% to 11% and used car rates around 11% to 14%. At this tier, pre-approval is especially important because dealer markup stacked on top of an already-elevated rate can push your effective rate into subprime territory even though your credit does not warrant it.

Subprime and deep subprime (below 600): Rates can range from 12% to 21% or higher. At this level, the cost of borrowing becomes a significant portion of the total vehicle cost. Buyers in this tier should carefully consider how much vehicle they can afford and whether a smaller loan on a less expensive car would produce a better long-term outcome. A car buying advocate can help structure the deal to minimize the total cost of borrowing.

How Dealer Rate Markup Works

When you finance through a dealership, the finance manager submits your credit application to multiple lenders. Each lender responds with a "buy rate," which is the actual interest rate the lender will accept based on your credit profile. The finance manager is not required to offer you that rate. Instead, they typically mark it up by 1% to 2.5% and present you with the higher number. The dealership keeps the difference as profit.

This practice is called "dealer reserve" or "finance reserve." It is legal in most states, and the dealer is not required to tell you the lender's original buy rate. The Consumer Financial Protection Bureau has flagged this practice as a source of significant consumer harm, noting that markup discretion disproportionately impacts minority and female borrowers and costs consumers tens of millions of dollars in excess charges each year.

Here is how it works in practice. If the lender approves you at 4.5% (the buy rate) and the finance manager marks it up to 6.5% (the sell rate), you are paying 2% more than you need to. On a $40,000 loan over 60 months, that 2% markup costs you approximately $2,200 in extra interest over the life of the loan. The markup does not appear as a line item. It is invisible. It is embedded in your monthly payment, and most buyers never know it is there.

Andrew Eder managed a dealership finance office before founding Rolo Rides. He structured these markups. He knows how they are calculated, how they are presented, and how they are justified internally. When Rolo Rides handles a deal, the financing is evaluated specifically for rate markup, and the buyer pays the actual lender rate, not an inflated version of it.

New vs. Used Car Loan Rates

Used car loans carry higher interest rates than new car loans, typically 1 to 3 percentage points higher across all credit tiers. The reason is risk: used vehicles depreciate faster, have higher repair costs, and present more uncertainty to lenders about future value and mechanical reliability.

In 2026, the average new car loan rate is approximately 7% while the average used car loan rate is approximately 11% to 12%, according to Experian. That gap is significant. On a $30,000 used car loan over 60 months at 11%, you would pay approximately $9,100 in total interest. The same loan at 7% would cost approximately $5,600 in interest, a savings of $3,500 just from the rate difference.

For used car buyers, this makes pre-approval even more critical. The higher the base rate, the more expensive dealer markup becomes in absolute dollar terms. A 1% markup on a 5% new car loan costs less than a 1% markup on a 10% used car loan because you are paying interest on a larger effective rate for the entire loan term.

Loan term also matters significantly. Stretching a used car loan from 60 months to 72 or 84 months lowers the monthly payment but increases the total interest cost substantially and raises the risk of being "upside down" (owing more than the vehicle is worth). Rolo Rides evaluates the complete financing structure on every deal, not just the rate, to ensure the loan term, down payment, and rate work together in the buyer's favor.

How to Get the Best Rate on Your Car Loan

Get pre-approved before visiting any dealership. A pre-approved loan from your bank or credit union establishes your actual rate before the dealer has any opportunity to mark it up. This is the single most important step in auto financing. If the dealer can beat your pre-approved rate through a manufacturer promotion, evaluate it. But you are comparing from a position of knowledge, not guessing.

Check your credit score before you apply. Knowing your score tells you which rate tier you fall into and what rates to expect. If your score is near a tier boundary (for example, 658 vs. 662), taking a few weeks to pay down a credit card balance or correct an error on your report could push you into a lower rate tier and save hundreds in interest.

Keep your loan term at 60 months or less. Longer terms reduce monthly payments but increase total interest cost and depreciation risk. A 72-month loan on a new car and an 84-month loan on a used car are warning signs that the vehicle may be too expensive for the buyer's budget at a sustainable payment level.

Negotiate the vehicle price before discussing financing. The dealership wants to combine price, financing, and trade-in into a single conversation because it is easier to hide profit when all three are blended. Negotiate the out-the-door price first. Lock it in writing. Then discuss financing. Then discuss trade-in. That sequence prevents the dealer from offsetting a price discount with a higher interest rate.

Have a professional review the financing. Rolo Rides evaluates the financing on every deal because Andrew Eder managed the room where rates are structured. He can identify markup, compare the dealer's offer against your pre-approval, and ensure the loan terms serve your interests, not the dealer's. That review is included in the flat $999 fee.

2026 Car Loan Rate Reference Table

| Credit Tier | Score Range | New Car Rate | Used Car Rate | Watch For |

|---|---|---|---|---|

| Super Prime | 781+ | 4.5% to 5.5% | 5.5% to 7% | Anything above 6% on new is likely marked up |

| Prime | 661-780 | 5.5% to 7.5% | 7% to 10% | Wide range means shopping lenders matters most |

| Near Prime | 601-660 | 8% to 11% | 11% to 14% | Markup can push rate into subprime territory |

| Subprime | 501-600 | 12% to 16% | 14% to 18% | Consider a smaller loan on a less expensive vehicle |

| Deep Subprime | Below 501 | 16%+ | 18% to 21%+ | Total interest may exceed the vehicle's value |

These ranges are based on Experian Q4 2025 data and Bankrate's 2026 survey data. Your actual rate depends on your specific credit profile, the lender, the vehicle, and whether the rate has been marked up by the dealership. Use this table as a reference when evaluating any offer. If your rate is significantly above the range for your credit tier, ask why.

Frequently Asked Questions

Q: Is 7% a good interest rate on a car loan in 2026?

A: It depends on your credit score. For a buyer with a credit score above 700, 7% is at or above the national average and may include dealer markup. For a buyer with a score in the 620 to 660 range, 7% would be a competitive rate. The rate itself is not good or bad in isolation. It is good or bad relative to what your credit profile should qualify you for. Pre-approval from your bank or credit union tells you what rate you actually deserve.

Q: How do I know if the dealer marked up my interest rate?

A: The most reliable way is to get pre-approved before visiting the dealer. If your credit union offers 5.2% and the dealer offers 7.2%, you know there is a 2% gap. The dealer may be able to beat your rate through a manufacturer promotion, but if the offered rate is higher than your pre-approval with no promotional explanation, markup is the likely cause. Dealers are not required to disclose the lender's original buy rate in most states.

Q: Should I finance through the dealer or my own bank?

A: Get pre-approved through your own bank or credit union first. Then let the dealer try to beat it. If the dealer offers a lower rate through a manufacturer promotional program, evaluate it on total cost (including any rebates you might forfeit by choosing promotional financing). A car buying advocate can run both scenarios and determine which option produces the lowest total cost for your specific deal.

Q: Does loan term affect my interest rate?

A: Yes. Shorter loan terms (36 to 48 months) typically carry lower interest rates than longer terms (72 to 84 months). Lenders charge more for longer loans because the risk of default increases and the vehicle depreciates further over a longer period. A 60-month loan is the most common term and generally offers a balance between manageable payments and reasonable total interest cost.

Q: How does Rolo Rides help with financing?

A: Rolo Rides reviews the financing on every deal as part of the flat $999 engagement. Andrew Eder evaluates the offered rate against pre-approval benchmarks, identifies any dealer markup, and ensures the loan term and structure serve the buyer's interest. Because Andrew managed a dealership finance office, he understands how rates are structured from the dealer's side and can identify markup that most buyers would never see.

Want to Learn More?

This guide combines current market data from Experian, Bankrate, and the Federal Reserve with direct dealership finance office experience from over 1,000 vehicle transactions. The rate ranges, markup explanations, and protection strategies reflect how auto lending actually works, not how it is described in generic financial advice.

Citations

- "State of the Automotive Finance Market — Q4 2025" — Experian reported average new car loan rates of 6.37% and average used car loan rates of 11.26% in Q4 2025. Super prime borrowers (781+) averaged 4.66%, while deep subprime borrowers averaged 16.01%. These figures represent the broadest available dataset of actual auto loan originations. https://www.experian.com/automotive/auto-finance-trends

- "Do Car Dealers Make Money on Financing?" — NerdWallet reports that an MIT analysis found 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points. This is the clearest evidence that the rate you are offered at a dealership is not the rate the lender actually approved. https://www.nerdwallet.com/auto-loans/learn/dealers-profit-off-financing

- "CFPB to Hold Auto Lenders Accountable for Illegal Discriminatory Markup" — The Consumer Financial Protection Bureau flagged dealer interest rate markup as a structural source of consumer harm affecting tens of millions of dollars in excess charges annually, with a disproportionate impact on minority borrowers. https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-to-hold-auto-lenders-accountable-for-illegal-discriminatory-markup/

Auto lending rates in 2026 are influenced by the Federal Reserve's rate decisions, lender competition, and vehicle market conditions. The Fed's current target rate of 3.50% to 3.75% provides the baseline for all consumer lending. Individual rates are then determined by creditworthiness, loan term, vehicle type, and whether the dealership has marked up the lender's offer.

A good interest rate is not a number you find on a chart. It is the rate your credit profile actually qualifies for, without dealer markup. The only way to know that number is to get pre-approved before you negotiate and to have someone who understands the finance office review the dealer's offer before you sign. Rolo Rides does both on every deal. If you are getting ready to buy and want to know what rate you should actually be paying, a free discovery call is the place to start.

Quality Verified

This content scored 92% in the Probably Genius Publication Readiness Assessment, meeting standards for direct answers, section depth, proof points, citation quality, and AI extractability.

About the Author

Andrew Eder is the founder of Rolo Rides, a flat-fee car buying advocacy service based in Austin, Texas. Before switching sides to represent buyers, Andrew spent five years inside four dealerships, including Honda, Mazda, and Lexus, where he worked in sales and managed the finance office. That experience gave him direct insight into how vehicles are priced, how interest rates are marked up, and how the finance office generates profit most buyers never see. Andrew holds a degree in Electrical Engineering from Milwaukee School of Engineering. He has facilitated over 1,000 vehicle transactions across 9 states and built Rolo Rides on a simple principle: charge the buyer a flat fee, accept zero compensation from the dealership, and protect every part of the deal.