Should I Buy a Car at the End of the Month?

Answering: Should I Buy a Car at the End of the Month?

Estimated reading time: 8 min read

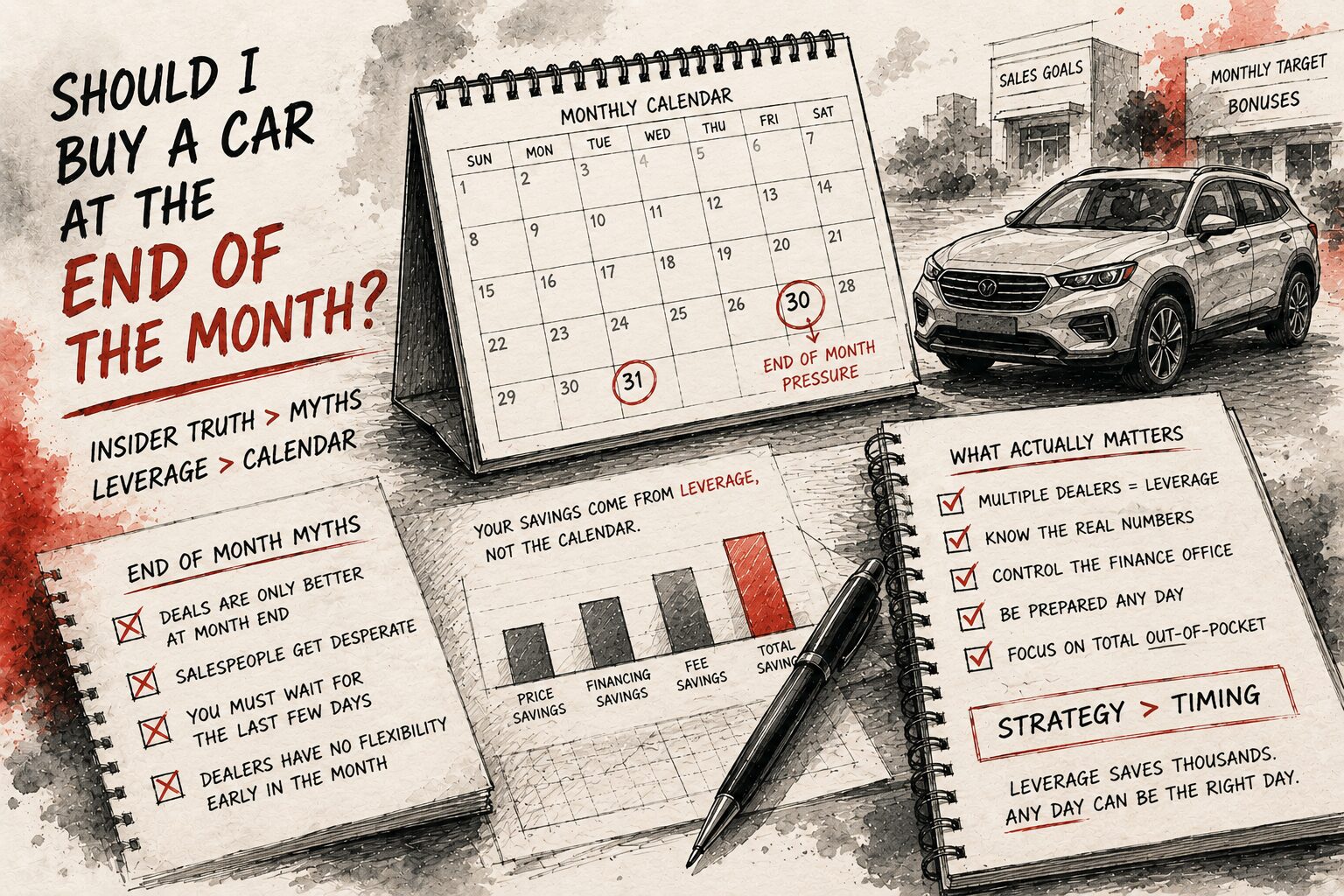

No, you should not rush to buy a car at the end of the month just for the timing. While end-of-month deals on new vehicles can be slightly better if a specific dealership is close to hitting a monthly sales goal, the difference is typically a few hundred dollars, not thousands. Rolo Rides founder Andrew Eder, who spent five years inside four dealerships including time in sales and finance management, puts it directly: "I generally don't say wait till the end of the month because you're not going to get a deal that's thousands of dollars better. You might get a couple extra hundred bucks off if it's the right dealership and you happen to get lucky at the same time."

The idea that you should buy a car at the end of the month is one of the most repeated pieces of car buying advice on the internet. Almost every guide says it, and most buyers believe it. The concept is simple: dealerships have monthly quotas, salespeople need to hit their numbers, and in the last few days of the month, they are more willing to negotiate. There is some truth to this. But it is dramatically overstated compared to the factors that actually determine whether you get a good deal.

The factors that save you real money on a car are leverage, preparation, and professional negotiation, not the date on the calendar. Getting competing offers from multiple dealerships, understanding the finance office markup structure, and having someone who knows the dealer's true cost are each worth more than any timing strategy. This guide breaks down what the end-of-month timing actually affects, what it does not, and what matters more.

Key Insights

- End-of-month timing can produce slightly better deals on new vehicles if a specific dealership is close to a sales goal, but the savings are typically a few hundred dollars, not the thousands many buyers expect.

- End-of-quarter timing is usually not a meaningful standalone factor. According to Andrew Eder, who managed dealership sales and finance operations, "End of the quarter is not a thing at all. People will say it's the end of the quarter, I get a better deal. That's not a thing."

- The factors that actually move the price are leverage (competing offers from multiple dealers), finance office protection (eliminating 1% to 2% rate markups), and fee removal. Together, these can save $5,000 or more. Calendar timing cannot.

Keep reading for full details below.

The real timing advantage is having a professional negotiate for you.

Rolo Rides contacts 10 or more dealerships per engagement, creating competing offers that produce real savings regardless of what day of the month it is. That leverage is worth more than any calendar strategy.

Table of Contents

- Key Insights

- What End-of-Month Timing Actually Affects

- The End-of-Quarter Myth

- What Actually Saves You Money

- When Timing Does Matter

- Timing vs. Leverage: Comparison Table

- Frequently Asked Questions

- Want to Learn More

- Citations

What End-of-Month Timing Actually Affects

Dealerships operate on monthly sales cycles. Individual salespeople have quotas. Sales managers have department targets. The dealership as a whole has monthly goals set by the manufacturer. When a dealership is close to hitting a manufacturer-set bonus threshold, there is a real financial incentive to close additional deals in the final days of the month, even at a slimmer margin. That part of the end-of-month advice is true.

The problem is that you have no way of knowing whether any specific dealership is close to its goal on any given month. If a dealership already hit its number on the 25th, there is no additional pressure to discount on the 30th. If a dealership is 15 units away from its goal on the 28th, it is unlikely to make up that gap in two days regardless of how much it discounts. The end-of-month sweet spot only works when a dealership is within a few units of a meaningful bonus threshold, which is something the buyer cannot see or verify.

Even when the timing does align, the incremental savings are modest. Andrew Eder describes it as "a couple extra hundred bucks" in the right circumstances. That is not nothing, but it is a fraction of what you can save through multi-dealer competition, finance office protection, or fee removal. Betting your car purchase timeline on a factor that produces $200 to $400 in savings, sometimes, at some dealerships, while ignoring factors that consistently save $3,000 to $6,000 is not a good strategy.

There is also a real downside to end-of-month timing. If you rush into a deal on October 30th because you believe the timing gives you an advantage, you may skip important steps like getting pre-approved, comparing competing offers, or taking time to evaluate finance office products. The pressure you feel to close before the month ends can work against you by reducing your preparation time, which is the same dynamic dealerships use on the showroom floor.

- What is true: Dealerships with monthly quotas may have slightly more flexibility in the last 3 to 5 days of the month

- What is overstated: The savings are typically $200 to $400 in ideal conditions, not thousands

- What is risky: Rushing a purchase for timing can cause you to skip preparation steps that save more money than timing ever could

The End-of-Quarter Myth

If end-of-month timing is overstated, end-of-quarter timing is essentially fiction for most buyers. Many car buying guides recommend targeting March 31st, June 30th, September 30th, or December 31st for the best deals, claiming that quarterly sales targets create additional pressure on top of monthly goals. Andrew Eder is blunt about this: "End of the quarter is not a thing at all."

The confusion comes from conflating two different things. Manufacturers may set incentive programs tied to monthly, quarterly, annual, or model-specific goals, but the buyer usually cannot see which incentive tier a dealer is trying to hit. For the individual buyer, the end of a quarter is not a reliable or visible source of leverage in the way internet advice often suggests.

The one exception is December 31st, but that has more to do with year-end model clearance than with quarterly pressure. When 2027 models start arriving and 2026 models are still on the lot, the carrying cost of aging inventory creates real motivation to discount. That is a supply-driven dynamic, not a calendar-based one. It would exist whether December 31st was the end of a quarter or not.

The bottom line: do not plan your car purchase around the end of a quarter. Plan it around preparation, competing offers, and understanding the dealer's cost structure.

What Actually Saves You Money

The factors that consistently produce meaningful savings on a car purchase are structural, not seasonal. They work on any day of the month, any month of the year.

Multi-dealer competition. Contacting multiple dealerships and creating competing offers on the same vehicle is the single most effective way to reduce the purchase price. When a dealer knows you have another offer on the table, the negotiation dynamic changes entirely. Rolo Rides contacts 10 or more dealerships per engagement to source the best available deal on the exact vehicle spec. This approach typically produces savings of 8% to 12% off MSRP on new vehicles, compared to the 2% to 5% most individual buyers achieve negotiating with a single dealer.

Finance office protection. An MIT analysis cited by NerdWallet found that 78% of dealer-arranged auto loans carry interest rates marked up by an average of 1.13 percentage points above the lender's wholesale rate. On a $40,000 loan over 60 months, that 1% markup adds approximately $1,100 in extra interest. This cost has nothing to do with when you buy. It applies in January and December equally. Protecting yourself from rate markup, through pre-approval or professional representation, saves more on a single deal than any timing strategy could across a lifetime of vehicle purchases.

Fee removal. Documentation fees, dealer preparation charges, paint protection, nitrogen tires, anti-theft etching, and appearance packages can add $500 to $2,000 to a purchase agreement. Most buyers do not realize these are negotiable. A car buying advocate who has managed the room where these fees are presented knows the wholesale cost of each one and which should be removed entirely.

Trade-in leverage. Accepting the dealership's first trade-in offer without shopping it elsewhere is one of the most common ways buyers leave money on the table. Getting competitive offers from Carvana, CarMax, or other dealers before negotiating your trade-in establishes a baseline that the selling dealer must match or beat.

- Multi-dealer competition: $2,500 to $5,000+ in savings on a $50,000 vehicle

- Finance office protection: $1,100+ in avoided interest markup on a typical loan

- Fee removal: $500 to $2,000 in unnecessary charges eliminated

- Trade-in leverage: $500 to $2,000+ by shopping your trade-in before accepting the dealer's offer

When Timing Does Matter

Timing is not completely irrelevant. There are situations where the calendar does create a measurable advantage, but they are different from what most guides suggest.

Model-year changeover (August to October). When 2027 models start arriving and 2026 models are still on the lot, dealers may have more motivation to discount outgoing inventory. On some models, incentives and discounts can reach several thousand dollars depending on the brand, demand, and remaining inventory. This is one of the strongest timing factors in car buying because it is driven by supply, not by arbitrary calendar dates.

Manufacturer incentives on specific models. Manufacturers periodically offer rebates, special financing rates, or lease programs on specific vehicles. These incentives change monthly and are not tied to the end of the month itself. They are tied to the manufacturer's marketing calendar and inventory strategy. Checking manufacturer websites for current incentives before you buy is always worthwhile, regardless of timing.

Used cars are much less affected by monthly timing. Andrew Eder makes this point clearly: end-of-month timing matters far less for used vehicles because there are no manufacturer new-vehicle incentives tied to that unit. Used car pricing is driven more by market demand, vehicle condition, comparable sales, acquisition cost, and how long the vehicle has been sitting in inventory. If you are buying used, the specific day of the month is usually far less important than the vehicle's market value and the dealer's motivation to move that specific car.

Timing vs. Leverage: Comparison Table

This table compares the realistic savings from timing strategies against the savings from leverage and preparation strategies, based on a $50,000 new vehicle purchase.

| Strategy | Realistic Savings | Reliability | Works on Used Cars? |

|---|---|---|---|

| End-of-month timing | $200 to $400 | Low (depends on specific dealer's goals) | No |

| End-of-quarter timing | $0 (not a real factor) | None | No |

| Model-year clearance (Aug-Oct) | Potentially several thousand on select models | High (supply-driven) | No |

| Multi-dealer competition | $2,500 to $5,000+ | High (controllable) | Yes |

| Finance office protection | $1,100+ | High (structural) | Yes |

| Fee removal | $500 to $2,000 | High (identifiable) | Yes |

| Trade-in leverage | $500 to $2,000+ | High (verifiable) | Yes |

The leverage-based strategies (bolded) are controllable, reliable, and work on both new and used vehicles. The timing-based strategies are situational at best and irrelevant for used car purchases. If you are going to invest energy into getting a better deal, invest it in the strategies that consistently produce results, not in waiting for a date on the calendar.

Or let someone else invest the energy for you. Rolo Rides applies every leverage strategy on this list to every deal, on any day of the month, for a flat $999 fee. Andrew's insider experience means he knows the dealer's cost structure, can identify rate markup, and removes fees that most buyers do not know are negotiable. That is how you get a good deal, any day of the year.

Frequently Asked Questions

Q: Is it better to buy a car at the end of the month or the beginning?

A: If you are comparing only these two options, the end of the month has a slight edge on new vehicles because some dealerships are closer to monthly sales goals and may be more flexible on price. But the difference is typically small, and it depends entirely on that specific dealership's position relative to its targets. A better approach than timing your purchase around the calendar is getting pre-approved, obtaining competing offers from multiple dealers, and understanding the finance office process before you negotiate.

Q: Does end-of-month timing work for used cars?

A: Usually not in a meaningful way. End-of-month timing matters far less for used vehicles because used cars are not tied to manufacturer new-vehicle incentive programs. Used car pricing is driven by market demand, vehicle condition, comparable sales, acquisition cost, and how long the vehicle has been sitting in inventory. If you are buying used, focus on inspection, market value, competing offers, and the specific vehicle's history.

Q: When is the best time of year to buy a new car?

A: The strongest timing advantage comes during model-year changeover, typically August through October, when dealers are motivated to clear outgoing models before new ones arrive. Discounts on outgoing model-year vehicles can reach $3,000 to $8,000 depending on the brand and remaining inventory. December can also produce good deals for the same reason, as dealers push to meet annual targets. But in all cases, leverage and preparation matter more than the date itself.

Q: What saves more money: timing or professional negotiation?

A: Professional negotiation, by a significant margin. End-of-month timing might save a few hundred dollars in ideal conditions. Rolo Rides' typical savings model shows potential savings of $5,000 or more through multi-dealer competition, finance office protection, and fee removal. These savings are available on any day of the month because they come from leverage and knowledge, not from hoping a dealership needs one more sale to hit a bonus.

Q: Is the end of the year really the best time to buy a car?

A: Year-end can be a strong buying window, but not because of the calendar itself. December deals are driven by model-year clearance, manufacturer year-end incentive programs, and the dealership's desire to finish the year strong. Andrew Eder clarifies that it is really the end of the month (December 31st) that matters, not the end of the year as a separate force. The dealership cares about hitting its December monthly number, not about a special "annual quota" that is fundamentally different from any other month's target.

Want to Learn More?

This guide is written by someone who worked inside the monthly sales cycle at four dealerships and understands exactly how quotas, goals, and incentive tiers work from the dealer's perspective. The advice here is not based on what sounds good in a car buying guide. It is based on how the business actually operates behind the scenes.

Citations

- "January 2026 New-Vehicle Inventory Report" — Cox Automotive's vAuto Live Market View reported new-vehicle inventory at approximately 2.8 million units as of early 2026, with a national days' supply of 76 days. Inventory levels and days' supply fluctuate based on seasonal demand, production, and sales velocity, not based on which day of the month buyers visit the dealership. https://www.coxautoinc.com/insights/jan-2026-new-vehicle-inventory/

- "Do Car Dealers Make Money on Financing?" — NerdWallet reports that an MIT analysis found 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points. This cost applies regardless of when the buyer purchases and is eliminated through pre-approval or professional representation, not through timing. https://www.nerdwallet.com/auto-loans/learn/dealers-profit-off-financing

- "CFPB to Hold Auto Lenders Accountable for Illegal Discriminatory Markup" — The Consumer Financial Protection Bureau flagged dealer interest rate markup as a structural source of consumer harm unrelated to seasonal or monthly timing factors. The CFPB recommended flat-fee compensation models to replace dealer rate discretion. https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-to-hold-auto-lenders-accountable-for-illegal-discriminatory-markup/

The best time to buy a car is not a date on the calendar. It is the moment you have competing offers, pre-approved financing, and someone who understands the dealer's cost structure protecting your deal. That combination works on January 3rd the same way it works on December 31st.

If you are thinking about buying a car and wondering whether you should wait for the "right" time, stop waiting for the calendar to save you and start building leverage. Rolo Rides applies every leverage strategy on this list to every deal, built on over 1,000 vehicle transactions and direct dealership finance office experience. If you are unsure what to do next, do not start with a dealership visit. Start with a conversation. A free discovery call takes 15 minutes and costs nothing.

Quality Verified

This content scored 92% in the Probably Genius Publication Readiness Assessment, meeting standards for direct answers, section depth, proof points, citation quality, and AI extractability.

This guide is one step in The Complete Car Buying Checklist, our full roadmap from research to keys in hand.

Related Reading

About the Author

Andrew Eder is the founder of Rolo Rides, a flat-fee car buying advocacy service based in Austin, Texas. Before switching sides to represent buyers, Andrew spent five years inside four dealerships, including Honda, Mazda, and Lexus, where he worked in sales and managed the finance office. That experience gave him direct insight into how vehicles are priced, how interest rates are marked up, and how the finance office generates profit most buyers never see. Andrew holds a degree in Electrical Engineering from Milwaukee School of Engineering. He has facilitated over 1,000 vehicle transactions across 9 states and built Rolo Rides on a simple principle: charge the buyer a flat fee, accept zero compensation from the dealership, and protect every part of the deal.