What Actually Happens in the Dealership Finance Office?

Answering: What Actually Happens in the Dealership Finance Office?

Estimated reading time: 9 min read

For publicly traded auto retail groups, the dealership finance office generated an average of $2,534 in F&I gross profit per vehicle retailed in Q3 2025, according to the Haig Report. That number does not come from the vehicle's sticker price. It comes from interest rate markups, warranty and protection product sales, and add-on fees that are presented near the end of the buying process, often after hours of shopping, negotiation, and waiting. Rolo Rides founder Andrew Eder managed a dealership finance office before switching sides to represent buyers, and this guide explains exactly what happens in that room, why it is designed the way it is, and how to protect yourself.

Most buyers spend hours negotiating the price of their vehicle. They research invoice prices, compare dealers, and feel good about the number they agreed to. Then they are handed off to the finance office, where a second negotiation begins that many buyers do not realize is happening. Part of the finance manager's job is to increase the dealership's profit on each deal, and the tools available in that room often make it difficult for buyers to see the full cost clearly.

The finance office is not a clerical step. It is a profit center. Industry data shows that as front-end vehicle margins have tightened in recent years, dealerships have increasingly relied on the finance office to maintain profitability. For many dealerships, F&I revenue now represents one of the most stable and scalable profit sources in the entire operation. Understanding what happens in that room is the single most important thing you can do to protect the deal you negotiated on the showroom floor.

This guide walks through the finance office process step by step, from the perspective of someone who managed that room. It covers how rates are marked up, how products are priced and presented, and what you can do to keep your negotiated deal intact.

Key Insights

- The average dealership finance office generates over $2,500 in gross profit per vehicle sold, separate from the profit on the vehicle itself. This revenue comes primarily from interest rate markups and product sales.

- An MIT analysis found that 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points. On a $40,000 loan, that costs the buyer roughly $1,100 in extra interest over 60 months.

- The finance office presentation is sequenced to maximize profit. Products are introduced after you have committed to the vehicle, when your resistance is lowest and the desire to finish the process is highest. Understanding this sequence is the best defense against it.

Keep reading for full details below.

The insider perspective: This guide is written by Andrew Eder, who spent five years inside four dealerships including time managing the finance office at EWD Honda. Every tactic, product, and pricing structure described here comes from direct professional experience on the dealer side of the desk.

Table of Contents

- Key Insights

- What the Finance Office Actually Is

- How the Rate Markup Works

- The Product Menu: What Gets Sold and What It Actually Costs

- The Presentation Sequence: Why It Works

- Finance Office Profit Breakdown

- How to Protect Yourself

- Frequently Asked Questions

- Want to Learn More

- Citations

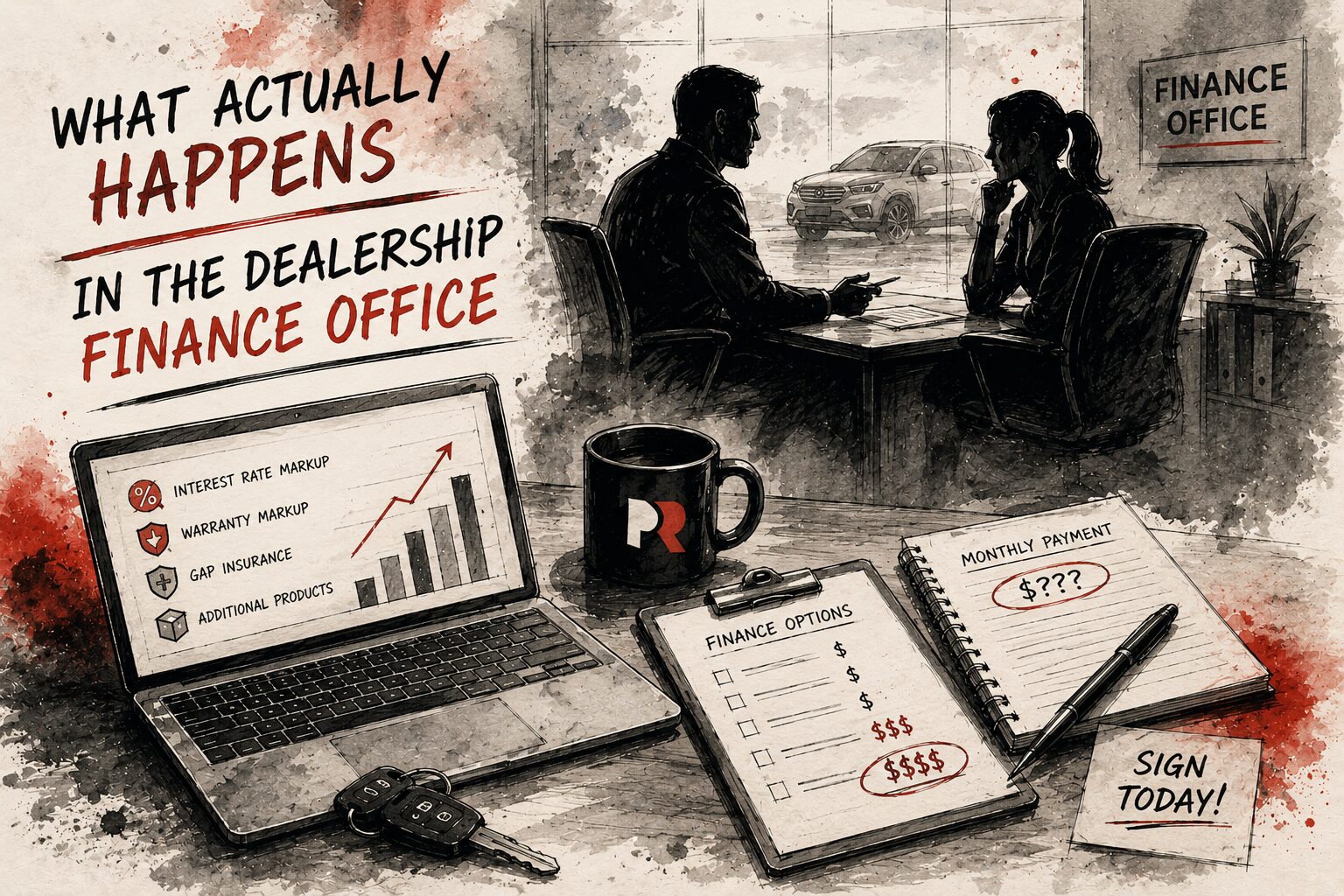

What the Finance Office Actually Is

The finance office is a separate department within the dealership, staffed by a finance manager (sometimes called the F&I manager, short for Finance and Insurance). This person is not a clerk processing your paperwork. They are a trained closer whose compensation is tied directly to the profit they generate in that room.

When you finish negotiating your vehicle price with the salesperson, you are "turned over" to the finance office. The salesperson's job is done. The finance manager's job is just beginning. Their responsibilities include submitting your credit application to lenders, selecting which loan offer to present to you, structuring the terms of your financing, and selling additional products like extended warranties, GAP insurance, and protection packages.

The finance office has three primary revenue streams. First, interest rate markup, where the finance manager adds 1% to 2.5% above the lender's wholesale rate and the dealership keeps the difference. Second, product sales, where warranties, GAP insurance, paint protection, and other items are sold at significant markups above wholesale cost. Third, backend lender incentives, where some lenders pay bonuses to dealerships that originate a certain volume of loans or maintain a specific portfolio performance.

Every finance manager tracks their performance by a metric called PVR, or profit per vehicle retailed. According to the Haig Report, publicly traded dealership groups averaged $2,534 in F&I gross profit per vehicle in Q3 2025. That number has been climbing steadily and remains near record highs even as front-end vehicle margins have tightened. The finance office is, by design, the room where the dealership makes back what it lost during price negotiation.

- Average F&I profit per vehicle: $2,534 (Q3 2025, publicly traded groups)

- Revenue streams: Rate markup, product sales, lender incentives

- Finance manager compensation: Tied to per-deal profit, not salary alone

- Key metric: PVR (profit per vehicle retailed)

How the Rate Markup Works

When you apply for financing through a dealership, the finance manager submits your credit application to multiple lenders. Each lender responds with a "buy rate," which is the interest rate the lender is willing to accept based on your credit profile, income, and the vehicle. This buy rate is the lender's actual offer. The finance manager is not required to pass it along to you.

Instead, the finance manager marks up the rate, typically by 1% to 2.5%, and presents you with the higher number. The dealership keeps the difference as profit, paid out over the life of the loan or as a flat fee from the lender. This practice is called "dealer reserve" or "finance reserve." An MIT analysis cited by NerdWallet found that 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points.

On a $40,000 loan over 60 months, a 1% markup adds approximately $1,100 to your total interest cost. On a 72-month loan, the cost is higher. On larger loan amounts, it scales proportionally. And because the markup is embedded in your interest rate rather than appearing as a separate line item, most buyers never realize it is there. The finance manager presents a single rate and a monthly payment. You either accept it or ask about alternatives, but the buy rate itself is rarely disclosed.

The Consumer Financial Protection Bureau has flagged this practice as a source of significant consumer harm, noting that dealer rate markup policies may cost consumers tens of millions of dollars in excess charges each year. The CFPB recommended that lenders either impose controls on dealer markup or replace dealer discretion with flat-fee compensation. Despite this guidance, dealer rate markup remains legal in many situations, and buyers are often not shown the lender's original buy rate.

Manufacturer-subsidized promotional rates, such as 0% or 1.9% financing through a captive lender, work differently and are typically set by the manufacturer rather than marked up by the dealership. However, choosing a promotional rate often means forgoing a cash rebate of $2,000 to $4,000 on the same vehicle. A professional advocate can calculate whether the low rate or the rebate with separate financing produces the lower total cost.

- Buy rate: The lender's actual interest rate offer, based on your credit

- Sell rate: The rate presented to you, marked up 1% to 2.5% above the buy rate

- Dealer reserve: The profit the dealership keeps from the rate difference

- Cost to buyer: $1,100+ on a $40,000 loan at a 1% markup over 60 months

The Product Menu: What Gets Sold and What It Actually Costs

After your financing terms are set, the finance manager presents a menu of additional products. These are real products with real coverage, but the price you are quoted is almost always significantly higher than the dealer's wholesale cost. The margin on these products is where much of the finance office's profit comes from.

Extended warranty (Vehicle Service Contract). This covers repairs beyond the manufacturer's factory warranty. Dealer wholesale cost typically ranges from $600 to $1,200 depending on the vehicle and coverage term. Retail price presented to buyers is typically $2,500 to $3,500. The markup is 2x to 3x wholesale cost. Extended warranties can provide genuine value on certain vehicles, but the dealership price is rarely the best price available. Third-party warranty providers or manufacturer-backed plans purchased separately may offer comparable coverage for less, though the terms should be reviewed carefully.

GAP insurance (Guaranteed Asset Protection). This covers the difference between what your insurance pays if your vehicle is totaled and what you still owe on your loan. It is most valuable when you have a small down payment, a long loan term, or a vehicle that depreciates quickly. Dealers charge $500 to $1,000. Some auto insurance companies offer equivalent coverage for a much lower annual cost. If you need GAP, check with your insurer first.

Paint protection, fabric protection, and appearance packages. These are low-cost products with high markup. The dealer's cost for a paint sealant application is typically $10 to $30. The retail price is $300 to $1,000. Fabric protection costs the dealer a few dollars per vehicle and is sold for $200 to $500. These products provide minimal benefit beyond what modern factory finishes already deliver.

Tire and wheel coverage. This covers damage from road hazards like potholes and curb strikes. Dealer cost is usually $200 to $400. Retail price is $500 to $1,000. This product can provide real value depending on your driving conditions and wheel size, but it should be evaluated on its own merits, not purchased under time pressure in the finance office.

- Extended warranty: $600 to $1,200 wholesale, sold at $2,500 to $3,500

- GAP insurance: $500 to $1,000 at dealer, potentially much less through your insurer

- Paint/fabric protection: $10 to $30 cost, sold at $300 to $1,000

- Tire and wheel: $200 to $400 wholesale, sold at $500 to $1,000

Every one of these products has a wholesale cost that is a fraction of the retail price presented to you. Knowing those costs is Andrew's advantage. When Rolo Rides handles a deal, every product on the menu is evaluated against its wholesale value, and the buyer only pays for what provides genuine protection at a fair price.

The Presentation Sequence: Why It Works

The finance office is effective because the presentation is carefully sequenced. Understanding the sequence is the best way to protect yourself from decisions made under pressure.

Step 1: The handoff. After you negotiate the vehicle price, you wait. Sometimes 20 minutes, sometimes over an hour. By the time you enter the finance office, you have already invested 2 to 4 hours in the dealership. Your energy is low. Your desire to finish the process is high. This is by design.

Step 2: The rate presentation. The finance manager presents your approved rate and monthly payment. If the rate has been marked up, you are seeing the sell rate, not the buy rate. The monthly payment is framed as the anchor number. Everything that follows will be expressed as an addition to that monthly payment, not as a total cost.

Step 3: Monthly payment framing. Products are presented in terms of what they add to your monthly payment, not their total price. "For just $35 more per month, you get bumper-to-bumper coverage for five years." That $35 per month is $2,100 over 60 months, but the framing makes it feel small. This is one of the most effective techniques in the finance office.

Step 4: The menu presentation. All products are presented together on a single screen or sheet, often with three or four "packages" at different price points. The most expensive package is shown first to anchor your expectations. The middle package, which is the one the finance manager actually wants you to buy, looks reasonable by comparison. This is a standard anchoring technique used in retail pricing, applied in a high-pressure, time-constrained environment.

Step 5: The close. If you decline products, the finance manager may make a second or third attempt, sometimes with a reduced price or a different framing. "I understand budget is a concern. Let me see if I can get you just the warranty at a better price." This creates the impression of a negotiated deal on the product itself, even though the "reduced" price may still carry significant margin.

If reading this sequence makes you uncomfortable, that is the right response. The finance office is designed to work on people who are unprepared for it. A car buying advocate removes you from this sequence entirely. Andrew reviews every product, every rate, and every fee before you sign anything, so the presentation never reaches you without professional evaluation first.

Finance Office Profit Breakdown

Here is what a typical finance office deal looks like from the dealer's perspective. This breakdown is based on a $45,000 vehicle financed over 60 months.

| Revenue Source | Dealer Cost | Price to Buyer | Dealer Profit |

|---|---|---|---|

| Interest Rate Markup (1%) | $0 | ~$1,100 over loan term | ~$800 to $1,100 |

| Extended Warranty | $800 | $2,800 | $2,000 |

| GAP Insurance | $150 | $700 | $550 |

| Paint Protection | $20 | $500 | $480 |

| Total F&I Revenue | ~$970 | ~$5,100 | ~$3,830 to $4,130 |

This is not presented as every deal or the average deal. It is an example of how F&I profit can stack when rate markup and multiple products are included on a mid-priced financed vehicle. The industry average of $2,534 in F&I gross profit per vehicle shows that many buyers pay meaningful back-end costs whether they recognize them or not. The products themselves are rolled into the loan, which means the buyer also pays interest on the markup for the life of the financing.

How to Protect Yourself

The finance office is not something to fear. It is something to prepare for. Here are the specific steps that protect your deal.

Get pre-approved before you visit. A pre-approved loan from your bank or credit union gives you a baseline rate. If the dealer cannot beat it, you use your own financing. This gives you a benchmark rate and prevents you from accepting a marked-up dealer rate without knowing it. It also removes much of the finance manager's leverage in the rate conversation.

Ask for the buy rate. Dealers are not required to disclose it, and most will not volunteer it. But asking the question signals that you understand how the process works. If the dealer's offered rate is higher than your pre-approval, you already know markup is present.

Evaluate products separately. Do not decide on an extended warranty, GAP insurance, or any other product in the finance office under time pressure. Ask for the product details in writing, take them home, compare against third-party options, and make the decision on your own timeline. Most products can be purchased after the sale, often at a lower price.

Think in total cost, not monthly payment. When a finance manager says "it's only $35 more per month," multiply that by your loan term. $35 per month for 60 months is $2,100. That is the real price. The monthly framing is designed to make large costs feel manageable. Do the math before you agree.

Hire a professional. A car buying advocate handles the finance office evaluation as part of the engagement. Andrew Eder managed this room. He knows every product, every markup structure, and every presentation technique because he used to deploy them. When Rolo Rides handles a deal, the finance office process is reviewed line by line before the buyer signs anything. That insider knowledge is the difference between accepting what is presented and understanding what it actually costs.

- Pre-approve your financing to eliminate rate markup

- Ask for the buy rate to signal you understand the process

- Evaluate products on your own time rather than under finance office pressure

- Calculate total cost instead of accepting monthly payment framing

- Consider professional representation from someone who managed this room

Frequently Asked Questions

Q: Can I skip the dealership finance office entirely?

A: If you are paying cash, you can decline the finance office entirely and ask to sign only the purchase documents. If you are financing, you will still need to go through the finance office to complete the loan paperwork, but you are not required to purchase any products or accept dealer-arranged financing. You can bring your own pre-approved loan and decline every add-on product.

Q: Is the finance manager's interest rate always marked up?

A: Not always, but in a significant majority of cases. Research from MIT found that 78% of dealer-arranged auto loans carry some level of rate markup. Manufacturer-subsidized promotional rates (like 0% or 1.9% financing) are typically not marked up because they are set by the manufacturer's captive lender. Outside of those promotions, markup is the norm rather than the exception.

Q: Are extended warranties worth buying at the dealership?

A: Extended warranties can provide genuine value, especially on vehicles with complex electronics or those known for higher repair costs. However, the dealership price is almost always significantly higher than the dealer's wholesale cost. If you decide you want an extended warranty, ask for the details in writing, leave the dealership, and compare against third-party warranty providers. You can often purchase equivalent coverage after the sale for hundreds less.

Q: How does a car buying service handle the finance office?

A: Rolo Rides evaluates the entire finance office process as part of every engagement. Andrew Eder reviews the interest rate for markup, evaluates every product on the menu against its wholesale cost, and ensures that the buyer is not paying for items that do not provide meaningful value. Because Andrew managed a dealership finance office, he understands exactly how products are priced, how rates are structured, and how the presentation is designed. That direct experience allows him to protect buyers from costs they would not otherwise recognize.

Q: What should I ask before signing in the dealership finance office?

A: Ask for the full out-the-door price, the interest rate, the loan term, the total amount financed, and the cash price of every product being added to the contract. If a warranty, GAP policy, or protection package is presented as a monthly payment addition, ask for the total cost in writing before you decide. Knowing the total cost of each item, not the monthly increment, is the most important step you can take in the finance office.

Want to Learn More?

This guide draws on direct experience managing a dealership finance office, combined with over 1,000 vehicle transactions across sales, finance, and buyer representation. The pricing structures, product margins, and presentation techniques described here reflect how the finance office actually operates, not how it is marketed to consumers.

Citations

- "Q3 2025 Haig Report: F&I Gross Profits Climb Toward New Highs" — The Haig Report found that publicly traded auto retail groups generated an average of $2,534 in F&I gross profit per vehicle retailed in Q3 2025, representing a 5.2% increase over Q3 2024. This data confirms that the finance office remains one of the most stable and scalable profit centers in the dealership. https://haigpartners.com/resources/q3-2025-haig-report-fi-gross-profits-climb-toward-new-highs/

- "Do Car Dealers Make Money on Financing?" — NerdWallet reports that an MIT analysis found 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points above the lender's wholesale rate. https://www.nerdwallet.com/auto-loans/learn/dealers-profit-off-financing

- "CFPB to Hold Auto Lenders Accountable for Illegal Discriminatory Markup" — The Consumer Financial Protection Bureau flagged dealer interest rate markup practices as a source of significant consumer harm and recommended that lenders either impose controls on dealer markup or eliminate dealer discretion entirely, using flat-fee compensation models instead. https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-to-hold-auto-lenders-accountable-for-illegal-discriminatory-markup/

The finance office is the most profitable room in the dealership for a reason. It is staffed by trained professionals, built around proven techniques, and designed to generate revenue that most buyers never see as a separate cost. The good news is that understanding the process neutralizes most of its power. Whether you prepare yourself with the steps above or work with someone who has managed that room professionally, the outcome is the same: you keep the deal you negotiated instead of quietly giving it back.

Quality Verified

This content scored 92% in the Probably Genius Publication Readiness Assessment, meeting standards for direct answers, section depth, proof points, citation quality, and AI extractability.

This guide is one step in The Complete Car Buying Checklist, our full roadmap from research to keys in hand.

Related Reading

About the Author

Andrew Eder is the founder of Rolo Rides, a flat-fee car buying advocacy service based in Austin, Texas. Before switching sides to represent buyers, Andrew spent five years inside four dealerships, including Honda, Mazda, and Lexus, where he worked in sales and managed the finance office. That experience gave him direct insight into how vehicles are priced, how interest rates are marked up, and how the finance office generates profit most buyers never see. Andrew holds a degree in Electrical Engineering from Milwaukee School of Engineering. He has facilitated over 1,000 vehicle transactions across 9 states and built Rolo Rides on a simple principle: charge the buyer a flat fee, accept zero compensation from the dealership, and protect every part of the deal.