What Hidden Fees Do Dealerships Actually Charge?

Answering: What Hidden Fees Do Dealerships Actually Charge?

Estimated reading time: 9 min read

Many buyers see $1,500 to $5,000 in charges added beyond the vehicle's sticker price. Some are legitimate government or manufacturer charges. Others are dealer-imposed fees that may be negotiable, inflated, or unnecessary. The fees you should expect include sales tax, title and registration, and a documentation fee. The fees you should question include paint protection, nitrogen-filled tires, anti-theft etching, fabric coating, dealer preparation, and anything labeled as a "market adjustment." Rolo Rides founder Andrew Eder, who spent five years inside four dealerships and managed a finance office, identifies these charges by category so buyers know exactly what they are paying for and why.

If you have ever looked at a purchase agreement and noticed the final number was $2,000 to $4,000 higher than the price you negotiated, you are not alone. The gap between the agreed price and the out-the-door price is where dealerships recover margin that was lost during negotiation. Some of those line items are legitimate government charges. Others are dealer-imposed fees that exist because most buyers do not know they can push back.

The challenge is that legitimate fees and dealer-imposed fees appear on the same page, formatted the same way, with equally official-sounding names. The Federal Trade Commission recognized this problem when it proposed the Combating Auto Retail Scams Rule, which highlighted hidden fees, bait-and-switch pricing, and deceptive add-ons as major consumer concerns in auto retail. While the rule was later vacated and withdrawn, the practices it targeted remain important warning signs for buyers reviewing a vehicle purchase agreement.

This guide breaks every common dealership fee into three categories: fees you must pay, fees you can negotiate, and fees you should refuse. It is written by someone who used to sit on the other side of the desk and knows exactly how each charge is calculated, justified, and presented.

Key Insights

- Government fees (sales tax, title, registration) are fixed and non-negotiable. Everything else on your purchase agreement is either set by the dealer or negotiable.

- Documentation fees range from $85 in California to over $1,000 in states with no caps. In Texas, the OCCC considers $225 the "presumed reasonable" limit, but dealers can charge more by filing a cost justification.

- The finance office is where the largest hidden costs appear. Interest rate markups of 1% to 2.5% above the lender's wholesale rate, warranty products sold at 2x to 3x wholesale cost, and last-minute "protection packages" can add $2,000 to $5,000 to your total cost without appearing as obvious fees.

Keep reading for full details below.

The quick test: If a fee is not a government charge (tax, title, registration) and it was not in the first price you were quoted, ask the dealer to explain what it covers and whether it can be removed. If they cannot clearly explain it, it may be worth challenging before you sign.

Table of Contents

- Key Insights

- Fees You Must Pay

- Ask for the Out-the-Door Price

- Fees You Must Pay

- Fees You Can Negotiate

- Fees You Should Refuse

- The Hidden Fee Most Buyers Miss: Finance Office Markup

- Dealership Fee Reference Table

- Frequently Asked Questions

- Want to Learn More

- Citations

Ask for the Out-the-Door Price

The easiest way to spot hidden fees is to ask for the out-the-door price before you visit the dealership or agree to a deal. The out-the-door price should include the vehicle price, taxes, title, registration, documentation fee, dealer add-ons, and any other charge required to complete the purchase.

If a dealer gives you only the monthly payment or only the advertised vehicle price, ask for a written buyer's order showing every line item. Hidden fees are much easier to challenge before you are sitting in the finance office. Comparing out-the-door prices between dealerships is the only reliable way to know which deal is actually cheaper, because a lower sticker price with higher fees can cost more than a higher sticker price with clean paperwork.

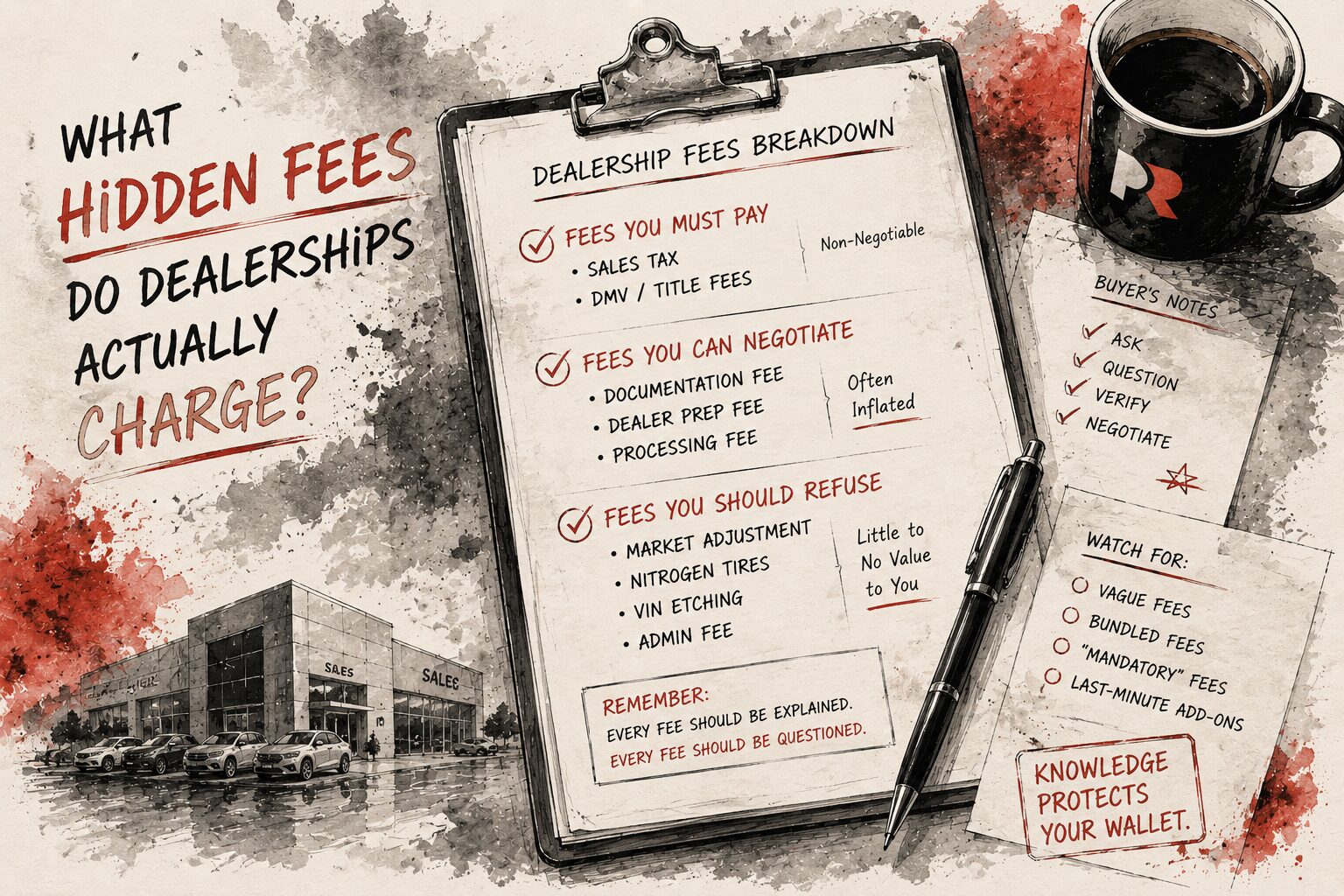

Fees You Must Pay

These are government-imposed charges that every buyer pays regardless of where or how they purchase a vehicle. They are not set by the dealership and they are not negotiable. Understanding them matters because they form the baseline of your out-the-door price, and any fee a dealer adds beyond these requires justification.

Sales tax. In Texas, the motor vehicle sales tax is a flat 6.25% of the purchase price. On a $50,000 vehicle, that is $3,125. This rate is set by the state and cannot be negotiated with the dealer. Some states calculate sales tax after manufacturer rebates are applied, others before. Texas applies tax to the full sale price minus any trade-in credit.

Title and registration. These fees cover the state's cost of transferring legal ownership and registering the vehicle in your name. In Texas, the title fee is approximately $33, and registration fees vary based on the county and vehicle type. These are paid to the state, not to the dealership. Some dealers charge a small processing fee on top of these for handling the paperwork on your behalf, which is usually lumped into the documentation fee.

Destination charge. On new vehicles, this is the manufacturer's charge for shipping the vehicle from the factory to the dealership. It is set by the manufacturer, printed on the window sticker, and generally consistent for the same model regardless of which dealer you visit. It typically ranges from $1,000 to $2,000 depending on the brand and where the vehicle was assembled. This fee is legitimate and standard on every new vehicle transaction.

- Sales tax (Texas): 6.25% of purchase price, minus trade-in credit

- Title fee (Texas): Approximately $33

- Registration: Varies by county and vehicle type

- Destination charge (new vehicles): $1,000 to $2,000, set by manufacturer

Fees You Can Negotiate

These fees are set by the dealership, not the government. They appear on nearly every purchase agreement, and while some cover real administrative work, the amounts are often inflated well beyond the actual cost of the service. The key principle: if the dealer set the amount, the dealer can change the amount.

Documentation fee. This is the most common dealer-imposed charge, covering the cost of preparing your purchase paperwork. In Texas, the Office of Consumer Credit Commissioner considers $225 the "presumed reasonable" limit. Dealers can charge above $225, but they must file a cost analysis with the OCCC to justify it. In other states, documentation fees are completely uncapped. Florida dealers routinely charge $899 to $1,200 for the same paperwork that costs $85 in California. While most dealers will not reduce their documentation fee directly (because they are required to charge the same amount to every customer), you can ask them to reduce the vehicle price by the same amount to offset a high fee.

Dealer preparation fee. Some dealerships charge $200 to $800 for "preparing" a new vehicle for delivery. On new cars, this work is already covered by the destination charge the manufacturer pays. The dealer is being compensated twice for the same work. If you see a separate preparation charge on a new vehicle, ask the dealer to explain what it covers that the destination charge does not. On used vehicles, a reasonable preparation fee covering detailing and inspection may be justifiable, but the amount should reflect actual work performed.

Advertising fee. Dealers in some regions share the cost of regional advertising through dealer associations. This fee, typically $200 to $500, sometimes appears as a separate line item. Whether you should pay it depends on context. If it was included in the original price quote, it is part of the negotiation. If it appeared only on the final purchase agreement, it is worth questioning.

- Documentation fee: $85 to $1,200+ depending on state. Texas presumed reasonable amount is $225.

- Dealer preparation fee: $200 to $800. Often duplicates work covered by destination charge on new vehicles.

- Advertising fee: $200 to $500. Regional cost-sharing that may or may not appear in your deal.

If sorting through which fees are negotiable and which are not feels overwhelming, that is a sign to bring in professional help. Rolo Rides reviews every line item on the purchase agreement before you sign, identifying which charges are legitimate and which should be reduced or removed. Andrew has been on the other side of that desk and knows exactly what each fee costs the dealer.

Fees You Should Refuse

These are charges that provide little or no value to the buyer and exist primarily to increase the dealership's profit margin. They are presented as standard, but they are almost always optional. A car buying advocate will identify and remove these before you sign anything.

Paint protection or sealant. Dealers charge $300 to $1,000 for a spray-on coating that costs them $10 to $30 in materials. Modern factory paint finishes are engineered to last years without aftermarket coatings. If you want professional paint protection film or ceramic coating, you will get a better product at a better price from an independent detailer after the purchase.

Fabric or interior protection. A $200 to $500 charge for a spray-on fabric protectant that costs the dealer a few dollars per vehicle. A $15 can of Scotchgard from any auto parts store provides equivalent protection. This fee is almost never worth paying at the dealership.

Nitrogen-filled tires. Some dealers charge $100 to $300 to fill tires with nitrogen instead of regular air. Nitrogen leaks slightly more slowly than air, but the practical benefit for everyday driving is negligible. Some warehouse clubs and tire shops offer nitrogen fills for free or at low cost. The FTC's CARS Rule specifically cited add-ons that do not provide a consumer benefit, such as nitrogen-filled tires on vehicles where the advantage is minimal, as the type of charge the rule was designed to address.

VIN etching or anti-theft etching. This involves etching your Vehicle Identification Number onto the windows, typically charged at $150 to $400. Kits to do this yourself cost under $30. While some insurance companies offer a small discount for VIN etching, the dealer's markup makes it a poor value proposition.

Market adjustment or additional dealer markup (ADM). On high-demand vehicles, some dealers add $1,000 to $10,000 or more above the manufacturer's suggested retail price. This is not a fee for any service. It is simply a price increase. It is negotiable, and many dealers in less competitive markets sell the same vehicle at or below MSRP. Sourcing the vehicle from a dealer that does not apply a market adjustment is often the most effective negotiation strategy.

- Paint protection: $300 to $1,000 for a $10 to $30 product. Skip it.

- Fabric protection: $200 to $500. A $15 can of Scotchgard does the same job.

- Nitrogen tires: $100 to $300. Free at Costco and many tire shops.

- VIN etching: $150 to $400. DIY kits cost under $30.

- Market adjustment: $1,000 to $10,000+. A price increase, not a fee. Always negotiable.

You can challenge these fees yourself, or you can have someone who used to present them challenge them for you. Rolo Rides removes unnecessary dealer add-ons as part of every engagement because Andrew knows the wholesale cost of each product and which ones provide real value versus dealer margin.

The Hidden Fee Most Buyers Miss: Finance Office Markup

The charges listed above appear as line items on your purchase agreement. But the single largest hidden cost in most car deals never appears as a fee at all. It is the interest rate markup applied in the dealership finance office.

When you finance through a dealership, the lender offers the dealer a wholesale "buy rate" based on your credit profile. The dealer is then allowed to mark up that rate by 1% to 2.5% and keep the difference as profit. An MIT analysis cited by NerdWallet found that 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points. On a $40,000 loan over 60 months, a 1% markup adds approximately $1,100 to your total cost. On longer loans of 72 to 84 months, the cost is even higher.

The Consumer Financial Protection Bureau has specifically flagged this practice, noting that dealer rate markup policies may result in tens of millions of dollars in excess costs to consumers each year. The CFPB recommended that lenders either impose controls on dealer markup or eliminate dealer discretion entirely, replacing it with flat-fee compensation. Despite this guidance, rate markup remains legal in most states, and dealers are not required to tell you the lender's original buy rate.

The finance office is also where warranty products, GAP insurance, and protection packages are sold, often at 2x to 3x the dealer's wholesale cost. Extended warranties that cost the dealer $800 are frequently sold for $2,500 to $3,500. GAP insurance may be available through some auto insurers for a much lower annual cost, while dealers often sell it for $500 to $1,000 as a one-time charge. These products are rolled into your loan, meaning you also pay interest on the markup itself.

Andrew Eder managed a dealership finance office before founding Rolo Rides. That experience gives him direct insight into both the sales-floor negotiation and the finance-office profit structure. He knows how rates are marked up, how products are priced, and how the presentation sequence is designed to maximize dealer revenue. When Rolo Rides handles a deal, the finance office process is evaluated as part of the engagement, ensuring buyers are not paying inflated rates or overpriced products.

- Rate markup: 1% to 2.5% above the lender's buy rate, adding $1,100+ on a typical loan

- Extended warranties: Sold at 2x to 3x the dealer's wholesale cost

- GAP insurance: $500 to $1,000 at the dealer versus $20 to $50 per year through your insurer

- Protection packages: Bundled add-ons combining several low-value products at a premium price

Dealership Fee Reference Table

Use this table as a quick reference when reviewing any purchase agreement. It covers the most common fees, typical cost ranges, and whether each charge is negotiable.

| Fee | Typical Range | Who Sets It | Negotiable? |

|---|---|---|---|

| Sales Tax (TX) | 6.25% | State | No |

| Title and Registration | $33 + county fees | State / County | No |

| Destination Charge | $1,000 to $2,000 | Manufacturer | No |

| Documentation Fee | $85 to $1,200+ | Dealer | Indirectly (offset via price) |

| Dealer Preparation | $200 to $800 | Dealer | Yes |

| Advertising Fee | $200 to $500 | Dealer / Regional | Sometimes |

| Paint Protection | $300 to $1,000 | Dealer | Yes (remove entirely) |

| Fabric Protection | $200 to $500 | Dealer | Yes (remove entirely) |

| Nitrogen Tires | $100 to $300 | Dealer | Yes (remove entirely) |

| VIN Etching | $150 to $400 | Dealer | Yes (remove entirely) |

| Market Adjustment (ADM) | $1,000 to $10,000+ | Dealer | Yes (source elsewhere) |

| Interest Rate Markup | 1% to 2.5% above buy rate | Dealer / Lender | Yes (pre-approve externally) |

| Extended Warranty | $2,500 to $3,500 (retail) | Dealer | Yes (negotiate or buy separately) |

| GAP Insurance | $500 to $1,000 (dealer) | Dealer | Yes (buy through insurer instead) |

Frequently Asked Questions

Q: Are dealer documentation fees negotiable?

A: Many dealers apply the same documentation fee across customers for compliance reasons, which means they may refuse to reduce the fee directly. However, you can ask the dealer to reduce the vehicle price by the same amount to offset a high fee. In Texas, the OCCC considers $225 the presumed reasonable limit for documentation fees on financed vehicles. If a dealer is charging significantly more, ask whether they have filed the required cost analysis with the state.

Q: How can I tell if a dealer fee is legitimate or invented?

A: Apply this test: Is it a government charge (tax, title, registration)? If yes, it is legitimate. Is it a manufacturer charge (destination)? If yes, it is standard. Is it a dealer-imposed charge that was not in the first price you were quoted? If yes, ask the dealer to explain what service it covers and whether it can be removed. Legitimate fees cover real administrative work. Invented fees cover things like paint sealant, nitrogen tires, or "delivery preparation" that duplicates work the manufacturer already paid for.

Q: What should I do if the final price is higher than the negotiated price?

A: Ask for a line-by-line breakdown of every charge on the purchase agreement before signing. Compare it against your original quote. Identify any charges that were not discussed during negotiation and ask the dealer to explain or remove each one. A car buying advocate reviews every line item as part of the engagement, ensuring that the price you agreed to is the price you actually pay.

Q: How does a car buying service handle dealer fees?

A: A car buying service like Rolo Rides reviews every fee on the purchase agreement before you sign. Andrew Eder identifies which charges are government-required, which are legitimate dealer costs, and which are inflated or unnecessary. Fees that do not provide value are negotiated down or removed entirely. Because Andrew managed a dealership finance office, he knows the wholesale cost of every product and the internal justification for every charge. That insider knowledge is the difference between accepting a fee and questioning it.

Q: Is it worth getting pre-approved for financing before visiting a dealership?

A: Yes. Pre-approval from your bank or credit union gives you a baseline interest rate that the dealer must beat or match. It removes the dealer's ability to mark up your rate without your knowledge and creates leverage in the finance office. Even if the dealer can offer a better rate through a manufacturer promotion, having your own pre-approval ensures you are comparing against a real number, not a marked-up one.

Q: What is an out-the-door price?

A: The out-the-door price is the total amount required to buy the vehicle, including the sale price, taxes, title, registration, documentation fee, dealer add-ons, and any other required charges. It is the number you should compare between dealerships because it shows the true cost of the deal. Always ask for the out-the-door price in writing before agreeing to any purchase.

Want to Learn More?

This guide draws on direct dealership experience across sales, finance management, and buyer representation totaling over 1,000 vehicle transactions. The fee categories, cost ranges, and negotiation strategies reflect how these charges actually work inside the dealership, not how they are described in marketing materials.

Citations

- "FTC Announces CARS Rule to Fight Scams in Vehicle Shopping" — The Federal Trade Commission identified hidden fees, bait-and-switch pricing tactics, and deceptive add-on charges as systemic consumer concerns in auto retail when it announced the CARS Rule in 2023. The rule was later vacated and withdrawn, but the FTC's original announcement remains useful as evidence of the consumer-protection concerns regulators identified in vehicle shopping. https://www.ftc.gov/news-events/news/press-releases/2023/12/ftc-announces-cars-rule-fight-scams-vehicle-shopping

- "Do Car Dealers Make Money on Financing?" — NerdWallet reports that an MIT analysis found 78% of dealer-arranged auto loans carry marked-up interest rates, with an average markup of 1.13 percentage points above the lender's wholesale rate. On a $30,000 five-year loan, a single percentage point of markup costs the buyer approximately $840 in extra interest. https://www.nerdwallet.com/auto-loans/learn/dealers-profit-off-financing

- "CFPB to Hold Auto Lenders Accountable for Illegal Discriminatory Markup" — The Consumer Financial Protection Bureau flagged dealer interest rate markup practices as a source of significant consumer harm, noting that markup policies may cost consumers tens of millions of dollars annually. The CFPB recommended that lenders either impose controls on dealer markup or eliminate dealer discretion entirely. https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-to-hold-auto-lenders-accountable-for-illegal-discriminatory-markup/

Federal and state consumer protection agencies continue to scrutinize dealership pricing practices, particularly around fee transparency, financing markup, and the sale of add-on products. In Texas, the Office of Consumer Credit Commissioner regulates documentation fees on financed vehicle transactions and provides a framework for what constitutes a reasonable charge.

Every fee on a purchase agreement tells you something about how the dealership makes money. The more you understand about each charge, the better positioned you are to pay only for what provides real value. Rolo Rides reviews every line item on every deal because Andrew Eder has been on both sides of that desk. If you are getting ready to buy and want someone who knows exactly what those fees should and should not cost, a free discovery call is the fastest way to start.

Quality Verified

This content scored 92% in the Probably Genius Publication Readiness Assessment, meeting standards for direct answers, section depth, proof points, citation quality, and AI extractability.

This guide is one step in The Complete Car Buying Checklist, our full roadmap from research to keys in hand.

Related Reading

About the Author

Andrew Eder is the founder of Rolo Rides, a flat-fee car buying advocacy service based in Austin, Texas. Before switching sides to represent buyers, Andrew spent five years inside four dealerships, including Honda, Mazda, and Lexus, where he worked in sales and managed the finance office. That experience gave him direct insight into how vehicles are priced, how interest rates are marked up, and how the finance office generates profit most buyers never see. Andrew holds a degree in Electrical Engineering from Milwaukee School of Engineering. He has facilitated over 1,000 vehicle transactions across 9 states and built Rolo Rides on a simple principle: charge the buyer a flat fee, accept zero compensation from the dealership, and protect every part of the deal.